On May 18, 2026, the criminal marketplace B1ack’s Stash published a new archive containing mill 2026-5-28 10:36:20 Author: www.d3lab.net(查看原文) 阅读量:63 收藏

On May 18, 2026, the criminal marketplace B1ack’s Stash published a new archive containing millions of compromised payment cards on a well-known underground forum. The release had an explicitly promotional purpose: driving traffic to the illegal market, reinforcing its reputation within the carding ecosystem, and, according to the threat actor’s own narrative, punishing sellers accused of reselling the same cards elsewhere.

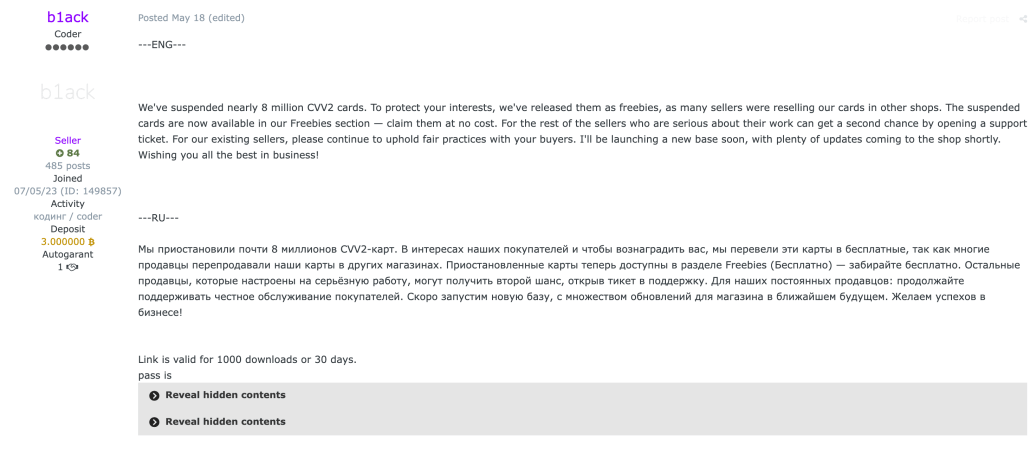

In the announcement, the threat actor claimed to have “suspended” almost 8 million CVV2 cards and made them available for free in the marketplace’s freebies section. The download link, distributed through Exploit.in’s Send platform, was limited to 1,000 downloads or 30 days.

A Criminal Marketing Operation

The free publication of large volumes of payment card data is not unusual in carding-focused marketplaces. The model is straightforward: release part of the inventory for free to generate attention, attract new registrations, demonstrate the alleged quality of the data, and push criminals toward purchasing newer or more targeted batches.

We had already observed a similar dynamic in February 2025, when B1ack’s Stash published a previous dataset presented as a mass free release. At the time, the analysis identified 1,018,014 unique cards, including 192,174 issued by European financial institutions. The May 2026 release therefore confirms a strategy already adopted by the marketplace: using public leaks as an advertising tool and as a positioning mechanism within the underground market.

Dataset Composition

The analyzed file contains 4,668,889 records. Each row follows a consistent 14-field structure separated by the pipe character (|):

PAN|expiration_month|expiration_year|CVV|name|address|city|state/province|postal_code|country|email|phone|IP|final_field

For ethical and security reasons, we do not publish any PAN, CVV, address, email, phone number, or personal data that could identify individuals.

The combined presence of PAN, expiration date, CVV2, personal details, billing address, email, phone number, and IP address is consistent with data collected through web skimmers or similar compromises of online payment flows. In e-skimming scenarios, malicious JavaScript code is injected into compromised checkout pages and intercepts the data entered by the user during the transaction.

The format observed in 2026 is partially different from the one analyzed in 2025: the previous release also included information such as date of birth and User-Agent, while the new dataset appears more standardized and focused on the resale of CVV2 cards.

Data Quality and Uniqueness

The analysis identified an extremely low number of duplicates:

| Metric | Value |

|---|---|

| Total records | 4,668,889 |

| Unique PANs | 4,668,887 |

| Duplicate PAN values | 1 |

| Duplicate records beyond the first occurrence | 2 |

From a formal card validation perspective, considering numeric PAN, compatible length, Luhn algorithm, expiration date, and CVV length, 4,659,138 records are formally valid, equal to 99.7911% of the dataset.

This does not mean that all cards are actually usable or still active. Formal validation only measures the syntactic and mathematical consistency of the data. Establishing whether a card is actually associated with an issuing institution, still active, or already known from previous compromises requires external enrichment, such as BIN/IIN validation and correlation with previous leaks.

A more restrictive metric, considering both a formally valid card and a complete record, results in 1,619,092 records, equal to 34.6783% of the dataset.

The main anomalies or incomplete fields identified are:

| Check | Non-compliant records | Percentage |

|---|---|---|

| Missing or invalid IP | 2,672,733 | 57.2456% |

| Missing or invalid email | 770,494 | 16.5027% |

| Missing phone number | 641,190 | 13.7332% |

| Missing postal code | 430,160 | 9.2133% |

| Missing state/province | 416,610 | 8.9231% |

| Missing address | 368,259 | 7.8875% |

| Missing city | 262,607 | 5.6246% |

| Missing name | 87,466 | 1.8734% |

| Invalid expiration date or expired card | 9,314 | 0.1995% |

| PAN failing Luhn validation | 339 | 0.0073% |

| Inconsistent CVV | 154 | 0.0033% |

Payment Networks Involved

The payment network distribution, estimated from the PAN, shows a clear prevalence of Visa and Mastercard:

| Payment network | Records | Percentage |

|---|---|---|

| Visa | 2,885,775 | 61.8086% |

| Mastercard | 1,498,617 | 32.0979% |

| American Express | 152,075 | 3.2572% |

| Discover | 124,533 | 2.6673% |

| Other/Undetermined | 7,889 | 0.1690% |

These figures are consistent with a dataset collected at global scale, with strong exposure of the payment networks most commonly used in online transactions.

Countries Involved

The country field in the dataset indicates the country associated with each record, most likely the billing or residence country provided during checkout. It should not automatically be interpreted as the country of the card issuer.

The main countries present in the dataset are:

| Country | Records | Percentage |

|---|---|---|

| United States | 3,242,564 | 69.4504% |

| Canada | 172,392 | 3.6924% |

| United Kingdom | 168,910 | 3.6178% |

| France | 131,260 | 2.8114% |

| Malaysia | 126,449 | 2.7083% |

| Australia | 50,466 | 1.0809% |

| Ireland | 50,166 | 1.0745% |

| Italy | 47,694 | 1.0215% |

| Spain | 45,208 | 0.9683% |

| Hong Kong | 39,902 | 0.8546% |

| Thailand | 36,609 | 0.7841% |

| Germany | 35,841 | 0.7677% |

| Switzerland | 35,607 | 0.7626% |

| Singapore | 35,419 | 0.7586% |

| India | 34,639 | 0.7419% |

The strong prevalence of the United States, accounting for approximately 69.45% of the dataset, combined with the presence of European countries and Asian financial hubs, suggests a collection that is not limited to a single local campaign but is compatible with multiple compromises of e-commerce websites or online payment flows.

Italy Focus

The dataset contains 47,694 records with the country set to ITALY, equal to 1.0215% of the full archive.

This subset was further enriched through BIN/IIN validation and correlation with previously known leaks. Based on this analysis, 18,026 Italian cards are valid and newly observed, meaning they are associated with a real issuing institution and had not previously been detected in other analyzed data leaks.

This equals 37.7951% of the Italian subset and 0.3861% of the full dataset.

Why the Dataset Is Consistent With Web Skimming Activity

Several elements point toward the web skimming hypothesis:

- complete payment data, including PAN, expiration date, and CVV2;

- billing and contact details;

- IP addresses associated with part of the records;

- structure compatible with information collected during an online transaction;

- broad geographic distribution, compatible with compromises across multiple e-commerce websites.

In a web skimming attack, criminals do not necessarily need to compromise a payment processor directly. It is enough to inject malicious code into a checkout page, a vulnerable plugin, a third-party script, or a component loaded by the website. The user completes the purchase and the payment may still succeed, but the data entered is also copied and sent to the attacker’s infrastructure.

Impact and Risks

The public release of an archive of this kind significantly increases the risk of abuse. Even when some cards have expired, have already been blocked, or are no longer usable, the criminal value of the dataset does not end with the PAN.

The dataset contains 3,916,423 records with an email address populated; among these, 3,898,395 email addresses are formally valid, equal to 83.4973% of the full archive. Unique valid email addresses total 3,393,269. This figure is important because it shows how the leak retains operational value even if a card has already been blocked or is no longer usable.

The same applies to personal and postal data: 4,253,304 records contain both a name and a street address, while 4,072,767 records include a more complete postal set made of name, address, city, postal code, and country. In 3,665,273 records, a formally valid email, a name, and a street address coexist. This combination enables abuse scenarios beyond payment card fraud, including phishing, vishing, targeted scams, unwanted physical mail, or unauthorized advertising campaigns.

The most critical aspect is the combination of financial and personal data. A single record may contain a card, name, address, email, phone number, and IP address: enough information to make a fraudulent communication significantly more credible.

Conclusions

The new B1ack’s Stash release is not just another payment card dump, but a concrete example of how criminal marketplaces use stolen data as a commercial lever.

Compared with the previous case analyzed in 2025, the volume observed in 2026 is significantly larger: 4,668,889 records, with 4,668,887 unique PANs and a formally valid card rate of 99.7911%. The Italian share, although minor within the full dataset, contains 47,694 records, of which 18,026 were found to be valid and newly observed after specific enrichment.

The nature of the data, its structure, and the presence of information collected during checkout make an origin from web skimming campaigns or similar compromises of e-commerce payment flows plausible. This confirms once again that online payment security cannot be limited to the backend: the attack surface also includes client-side code, third-party scripts, plugins, and dynamically loaded components on payment pages.

The phenomenon remains relevant not only for issuers and payment networks, but also for merchants, technology providers, and end users.

如有侵权请联系:admin#unsafe.sh